- DeFi Dev Corp. (Nasdaq: DFDV)

- Posts

- Every Agent Needs a SOL: Sizing the Opportunity for Agentic Finance on Solana

Every Agent Needs a SOL: Sizing the Opportunity for Agentic Finance on Solana

As AI agents begin to trade, pay, and transact autonomously, they will need a financial system built for machines. We believe Solana is emerging as the settlement layer for that future.

AI agents are quickly moving from science fiction to real economic actors. Instead of humans clicking buttons on apps, software will increasingly make decisions, execute trades, purchase services, and interact with financial systems on its own. These agents will need a way to hold assets, move money, and settle transactions autonomously. In other words, they need a financial system built for machines. We believe this system is Solana.

In our most recent report, “SOL & the Digital City: A New Way to Value Layer 1 Tokens,” we identify four major long-term demand drivers that are set to catapult Solana’s native token (SOL) to $10,000:

Real-world asset settlement collateral

Stablecoin settlement reserves

Agentic AI

Consumer demand

This report focuses on the third category: agentic AI. Our base-case estimate is that the emerging agent economy could generate roughly $27 billion in structural demand for SOL. The reason is simple. As autonomous agents transact onchain, they require working capital to operate, whether for gas, priority fees, DeFi interactions, or operational balances. Individually, the amount of SOL required per agent is small. But when multiplied across millions, and eventually potentially billions, of agents operating simultaneously, the aggregate demand becomes meaningful.

The key variable is not how much SOL each agent holds. It is how many agents exist. If AI agents scale into a global economic layer, buying data, paying for APIs, trading assets, managing liquidity, and interacting with decentralized applications, the number of agents transacting onchain could grow extremely large. Even modest working capital requirements per agent compound rapidly at that scale.

In this report, we explore why agents are likely to transact on public blockchains, why Solana’s speed and cost structure make it a natural settlement layer for machine-driven finance, what early data already exists today, and how different assumptions about the size of the agent economy translate into potential demand for SOL.

What is Agentic AI?

AI agents are software systems that use AI to pursue goals and complete tasks on behalf of users. They show reasoning, planning, and memory, and have a level of autonomy to make decisions, learn, and adapt. This is distinct from:

Chatbots, which respond to prompts but don’t act

Copilots, which suggest actions but require human confirmation

Traditional bots, which follow hard-coded rules without reasoning.

What makes the current generation of agents different from prior automation is the underlying model capability. Large language models like Claude Opus 4.6 and GPT-5 can now interpret ambiguous instructions, decompose complex tasks into subtasks, call external tools, recover from errors, and improve through feedback. These models turned a theoretical concept into a practical one. A year ago, “agents” were mostly demos. OpenClaw, an open-source agent framework that went viral in January 2026, surpassed 250,000 GitHub stars in March 2026 and 20,000 forks within weeks of its breakout. Andrej Karpathy called it “the most incredible sci-fi takeoff-adjacent thing,” as evidenced by a subsequent global shortage of Mac Minis as developers raced to build always-on agent servers, according to Axios.

How Agents Work: The Perception-Reasoning-Action Loop

At its core, every AI agent operates in a cycle. It perceives its environment (reads data, receives a message, observes a price feed). It reasons about what to do (the LLM processes context and decides on a plan). It acts (calls a tool, sends a transaction, writes a file). Then it observes the result and loops again. This is not a new concept in computer science, but what has changed is that the “reasoning” step is now performed by a foundation model that can handle ambiguity, context, and multi-step planning. Earlier bots operated on if/then logic. Agents operate on judgment.

This distinction matters for crypto because agents can now interact with DeFi protocols, manage wallets, execute trades, and pay for services without human intervention. With these capabilities, the key question is how much economic activity they will actually drive in the future.

Why Would Agents Transact Onchain?

This is the most important fundamental question, because if the answer is “they wouldn’t,” then the entire demand bucket in our model is zero. We see four structural reasons why autonomous agents will transact on public blockchains, and in particular, Solana.

Programmable Money Without Gatekeepers

Traditional payment rails were designed for humans. They require accounts, identity verification, authorization flows, and settlement delays. An AI agent has no identity document, no bank account, and no credit card. Can agents use traditional rails like Stripe? Technically, yes. An agent can be provisioned with API keys, linked to a corporate billing account, and programmed to authenticate through OAuth flows. But each of these steps introduces friction, latency, and a human dependency. Someone has to create the Stripe account, pass KYC, issue the API key, and manage the billing relationship. For a single agent, this is manageable. For ten million agents operating autonomously across organizational boundaries, it becomes a serious bottleneck. Public blockchains eliminate this friction entirely. An agent can hold assets in a self-custodial wallet, receive USDC, pay for a service, and settle in under a second on Solana. This can happen without registering with a payment processor, authenticating through a third party, or waiting for batch settlement. The advantage is not absolute (traditional rails work for tightly controlled enterprise agents), but it scales better as the number and diversity of agents grow.

The Internet Needs a Native Payment Layer

When Tim Berners-Lee designed HTTP in 1991, he reserved a status code for payments: HTTP 402, “Payment Required.” It was never implemented. Thirty-five years later, the internet still has no built-in way for one machine to pay another. Every payment on the web is bolted on top of credit card forms, subscription management platforms, OAuth flows, or invoicing systems. These layers were designed for humans buying things from businesses. They don’t work very well for software paying for software.

For agents, this is a foundational problem. An agent that needs to buy data from an API, pay for compute, or compensate another agent for a service currently has no native way to do so over the internet. For the most part, agents need to route through a payment system designed for a human sitting at a keyboard. Public blockchains fix this by making value transfer as programmable and composable as data transfer already is. An agent can send USDC to another agent’s wallet in a single transaction, settled and final in under a second, with no intermediary, no form to fill out, and no settlement delay.

The x402 protocol is the clearest evidence that this gap is being closed. Developed by Coinbase’s platform team and now governed by the independent x402 Foundation (co-established with Cloudflare), x402 finally implements the HTTP 402 status code as a real internet-native payment standard (x402.org). A server responds with payment requirements. The client authorizes a stablecoin transfer onchain and retries. Settlement occurs on Solana in ~400ms with no accounts, subscriptions, or API keys. Through February 2026, x402 has processed over 170 million cumulative transactions across supported chains, with roughly $200M in annualized payment volume in December 2025, according to Coinbase (note: this is an annualized run rate based on December activity; cumulative all-time volume through February 2026 was ~$45.9M per Artemis, reflecting a dropoff in January and February).

Speed Matters

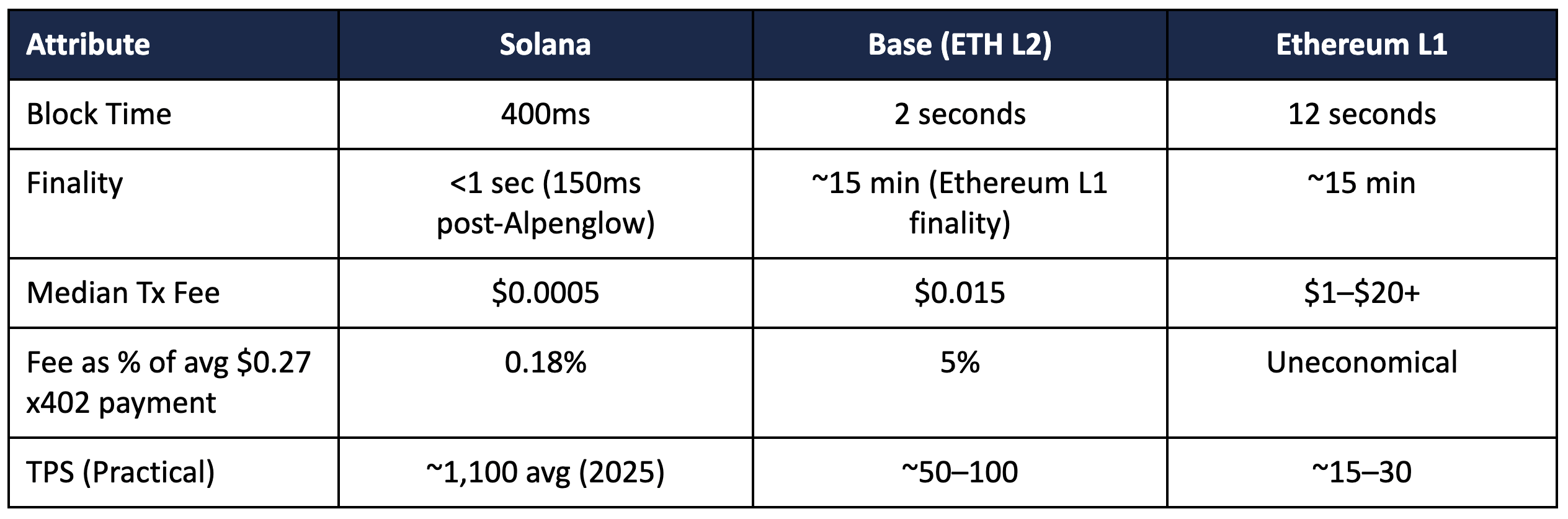

Agents operate in tight feedback loops: perceive, reason, act, observe. Each cycle requires waiting for transaction confirmation before the agent can move to the next step. On a 12-second block-time chain, a three-step workflow means 36+ seconds of dead time. On Solana, the same workflow is confirmed in under two seconds. A trading agent scanning for arbitrage opportunities needs to read a price, execute a swap, and confirm settlement before the opportunity closes. An agent procuring data via x402 needs to pay and receive the response within a single HTTP timeout window. In both cases, the chain that confirms fastest is the chain the agent will use. Solana’s 400ms block times and sub-second finality (targeting ~150ms post-Alpenglow) make it the lowest-latency settlement layer available. Speed may matter less for a human refreshing a browser, but it’s table stakes for agents making thousands of decisions per hour.

Cost Structure That Enables Micropayments

Solana’s median transaction fee is approximately $0.0005, per TokenTerminal. Stripe charges roughly $0.30 per transaction. PayPal charges $0.49 plus a percentage. Standard Chartered’s Geoffrey Kendrick noted that even Base, Coinbase’s Ethereum L2, has average gas fees of $0.015, meaning transaction costs consume 25% of an average x402 payment of $0.06. On Solana, that overhead drops to approximately 0.8%. At these levels, micropayments become viable. Agents paying fractions of a cent for API calls, data feeds, and compute become economically rational.

The Data That Exists Today

The agentic economy on Solana is nascent, but it is not hypothetical. Below is what we can actually measure.

A few important caveats on the above data. The $31B AI agent DEX volume figure from the Solana Annual Review likely includes volume on AI-associated tokens (e.g., $AI16Z, $GOAT) in addition to volume initiated by truly autonomous agents. The number is directionally useful as evidence of market interest, but it overstates the share of economic activity driven by agents acting independently. We use it as a ceiling, not a precise measurement.

The x402 data is cleaner as evidence of autonomous machine-to-machine activity, but it contains its own inconsistencies. 170 million cumulative transactions at $45.9M cumulative volume implies an average transaction size of roughly $0.27, not the $0.06 micropayment figure cited by Standard Chartered’s Kendrick. This likely reflects a small number of high-value transactions pulling the average up. Additionally, Artemis has developed a methodology to separate “real” from “gamed” x402 transactions (filtering out self-dealing and wash trading). At peak activity in late November 2025, over 78% of x402 transactions and 98% of volume were classified as non-organic. The gamed transaction share has since declined below 50%, but it means the cumulative headline figures significantly overstate genuine economic activity. The most credible signal comes from the real transaction trend: daily real x402 transactions averaged roughly 1.4 million in December 2025, fell to 740,000 in January 2026, and declined to roughly 180,000 in February (Four Pillars, citing Artemis).

It’s still early, but Solana is gaining traction. Through February 2026, Solana captured 27%+ of all x402 transactions on a cumulative basis. When filtered for real (non-gamed) activity, Solana’s share rose to approximately 82% of real x402 transactions in February 2026 (Four Pillars). These figures may be shocking to some but they’re hardly a surprise to us. Speed, cost, and developer tooling (Solana Agent Kit, ElizaOS, GOAT framework) have made Solana the default settlement layer for autonomous agents.

Solana’s Agent Infrastructure

Solana has assembled the most complete developer stack for onchain AI agents of any blockchain. The following frameworks are just a few of the ones that exist today.

Solana Agent Kit (SendAI): An open-source toolkit providing 60+ pre-built actions across token operations, NFT minting, DeFi interactions, and more. Supports LangChain, Vercel AI SDK, and MCP integration. Modular plugin architecture lets developers install only the capabilities they need (GitHub).

ElizaOS (formerly ai16z): An AI framework combining multiple applications and data layers into persistent “characters” that interact across platforms (X, Telegram, Discord) while executing onchain actions on Solana. Ideal for social agents requiring a persistent identity.

GOAT (Crossmint): A universal adapter providing a unified interface across 30+ chains, including Solana, with 200+ protocol plugins. Designed for agents that need cross-chain operability.

x402 Protocol: The HTTP-native payment layer backed by Coinbase, Cloudflare, Google, and Vercel. Enables per-request monetization of any API or service. Supported by a growing ecosystem of facilitators, including PayAI Network (Solana-first) and t54 for identity and risk management (Coinbase Docs).

This infrastructure is important because it reduces the integration cost for developers building agents. The concentration of agent-specific frameworks on Solana (five major toolkits, each with native DeFi protocol integrations) is unmatched by any single competing chain, even if comparable individual tools exist elsewhere in the EVM ecosystem.

Why Solana Over Ethereum L2s?

The most common pushback on Solana’s dominance in the agent stack is that Ethereum L2s (particularly Base, Arbitrum, and Optimism) can serve the same function.

Base, in particular, has a natural distribution advantage as the home chain of Coinbase, which developed x402. So why would agents choose Solana? We see four structural reasons.

Finality Is the Product

For an agent operating in a perception-reasoning-action loop, every transaction confirmation is a blocking step. On Solana, the agent waits <1 second. On Base, the transaction appears to confirm in ~2 seconds, but true finality (the point at which the transaction cannot be reverted) depends on Ethereum L1 settlement, which takes approximately 15 minutes. For agents managing DeFi positions, executing arbitrage, or competing for execution priority, this distinction matters. A trade that is not truly final is a trade that can be reorganized. Solana’s single-layer finality eliminates this ambiguity. Post-Alpenglow, Solana targets ~150ms finality, which is effectively real-time for any agent workflow.

Cost at the Margin

At $0.015 per transaction, Base’s gas fees consume 5% of the average x402 payment ($0.27). Solana’s $0.0005 median fee reduces that overhead to 0.18%. This delta is significant for agents making thousands of micropayments per day. Relayers and facilitators optimizing for cost will naturally gravitate toward the cheapest settlement layer, which is Solana by a factor of over 25x.

Composability Without Bridging

An agent on Solana can call Jupiter for a swap, deposit into a Marinade staking pool, and pay for an x402 API call in a single atomic transaction flow, all without bridging assets between layers. On Ethereum, an agent interacting with both L1 DeFi and an L2 must bridge between them, introducing latency, fees, and bridge risk. For agents that need to interact with the full DeFi stack (trading, lending, staking, LP provisioning), Solana’s single-layer composability is a significant operational advantage.

Developer Tooling Moat

Solana has the deepest collection of agent-specific frameworks. The Solana Agent Kit alone provides 60+ pre-built actions. ElizaOS enables persistent agent characters across social platforms. These tools lower the integration cost for developers, which creates a self-reinforcing cycle: more tools attract more developers, which attracts more agents, which generates more SOL demand.

Third-Party Market Sizing

There is no consensus on the size of the agentic AI market, but the range of estimates is directionally useful for calibrating our model. Below is a summary of the most credible third-party forecasts.

Two distinctions matter here. The first cluster (MarketsandMarkets through MarkNtel Advisors) measures the AI agent software and services market. This is revenue generated by agent platforms, infrastructure, and tooling vendors. These estimates cluster around $47–53B by 2030. The second group (Bain, Morgan Stanley, McKinsey) measures the total economic activity agents influence or execute, which is dramatically larger. Bain estimates $300–$500B in U.S. agentic commerce alone by 2030. McKinsey projects $3-5T in global agentic commerce revenue by 2030. Notably, McKinsey's figure covers B2C retail goods only and does not include services, B2B, or financial transactions. The total economic activity driven by agents across all verticals would be larger.

For the DFDV model, the second cluster is more relevant because we are sizing the total economic throughput that agents will produce onchain, not the revenue of agent software vendors. Our model’s $2T “full maturity” figure for the global AI agent economy sits well within the range when you extend Bain and Morgan Stanley’s US-only figures to a global basis and project beyond 2030.

Sizing SOL Demand: A Revised Framework

Our base case in the DFDV model derives $27B in structural SOL demand from the agentic economy using the following chain: $2T global AI agent economy × 30% moves onchain × 30% settles on Solana × 15% held as SOL = $27B.

A note on what $27B represents: this is a steady-state working capital figure, not an annual flow. It estimates the aggregate amount of SOL that agents must hold at any given time to fund gas, priority fees, DeFi positions, account rent, and operational float. The relevant analogy is the float in a payments network: Visa’s merchants don’t hold Visa’s total annual volume. They hold the working capital required to operate within the network at any given moment. Similarly, agents don’t hold $27B in SOL because they spend $27B per year. They hold $27B because, across millions of agents operating simultaneously, that is the aggregate SOL balance required to keep agentic finance up and running. The faster agents cycle through transactions (higher velocity), the less float each one needs; however, the number of agents grows simultaneously, keeping aggregate demand stable or growing.

Below, we pressure-test each variable and present bear, base, and bull cases.

Variable 1: Total Agent Economy ($2T)

Our base case assumes $2T. For context, Bain projects $300–500B in U.S. agentic commerce alone by 2030. Notably, this figure covers only retail shopping, not financial services, enterprise SaaS automation, infrastructure payments, or agent-to-agent services. Morgan Stanley projects up to $385B in U.S. e-commerce alone. McKinsey estimates agentic commerce revenue could reach $3-5T in 2030. Extending these figures globally and across all economic verticals, $2T represents a moderate assumption, not an aggressive one.

Bear: $500B (agents remain niche, limited to financial trading and developer tooling).

Base: $2T (agents penetrate commerce, finance, infrastructure, and enterprise workflows broadly).

Bull: $5T (every SaaS product, API, and application embeds agentic capabilities; agent-to-agent commerce scales rapidly).

This is the most difficult variable in the framework to calibrate because it requires forecasting how much of the agent economy will settle on public blockchains versus traditional payment rails. We derive our 30% estimate through two approaches and hold it constant across all cases.

Top-down: We use stablecoins as a starting baseline. McKinsey and Artemis Analytics published a joint study in early 2026, separating real stablecoin payment volume from trading and rebalancing noise. Their finding: actual stablecoin payments reached approximately $390 billion in 2025, doubling from 2024 (McKinsey). That $390 billion remains a small fraction of total global payment flows, but the differential in growth rates is what matters. Stablecoin payment volume grew 100% year-over-year while traditional digital payments grew roughly 8% (Statista). Agent-native protocols like x402 should further widen that gap. Agents don’t have credit cards or bank accounts and face zero switching costs across payment rails. They will default to whatever settles fastest and cheapest. The trajectory of onchain payment adoption is steepening, not flattening, and agents are the user base most likely to accelerate it.

Bottom-up: We segment agent activity by settlement requirement. Not all agent spending needs a blockchain. Enterprise agents operating within walled gardens (Salesforce automating a sales workflow, ServiceNow routing an IT ticket) will settle through corporate billing or internal ledgers. But three categories of agent activity structurally require permissionless settlement:

Intra-enterprise automation (~5% onchain): These agents operate inside corporate perimeters (i.e., automating CRM workflows, routing support tickets, generating internal reports). The transactions they produce (if any) settle through existing corporate billing, ERP systems, or internal ledgers. For example, there is no structural reason for a Salesforce agent talking to a ServiceNow agent within the same company to touch a public blockchain. The 5% probability estimate captures edge cases where an enterprise agent needs to interact with an external onchain service.

Cross-organizational agent-to-agent payments (~60% onchain): When two agents from different organizations need to transact—Company A’s procurement agent paying Company B’s fulfillment agent—there is no shared payment rail between them. Traditional options (ACH, wire, invoice-net-30) are slow, require human approval, and weren’t designed for machine-speed settlement. Permissionless blockchains are the lowest-friction option for settling between parties that don’t share a banking relationship. We discount from 100% because some cross-org activity will still route through platform intermediaries (e.g., two agents transacting within an Amazon or Shopify marketplace).

Micropayment-dependent services (~70% onchain): Card networks charge fixed per-transaction minimums of $0.20-0.30 plus 1-3%+ of the value. The average x402 payment is $0.27. Any agent activity priced in fractions of a cent (i.e., per-query API calls, per-token data feeds, per-inference compute) is economically impossible on traditional rails. Onchain micropayments are the only viable settlement mechanism at this price point. The 30% discount reflects that some micropayment use cases will be bundled into subscription or credit-based models that avoid per-transaction settlement entirely.

DeFi-native agents (~100% onchain): MEV bots, liquidation agents, LP managers, and yield optimizers are onchain by definition. Their entire operating environment is a blockchain. There is no off-chain alternative for these activities. The only question is how large this segment becomes relative to the total agent economy.

The raw bottom-up math suggests 46%, but we haircut it to 30% for three reasons. First, our segment share estimates are imprecise. If intra-enterprise automation proves larger than 40%, the blend drops. Second, hybrid solutions will likely emerge where agents initiate onchain but settle through traditional rails on the backend (e.g., stablecoin-to-fiat offramps). Third, regulatory friction in certain jurisdictions will slow onchain adoption even where the economics strongly favor it.

Regardless, the two approaches tell a consistent story: the top-down trajectory points to onchain payments gaining share rapidly from a small base, and the bottom-up segmentation estimates that roughly 60% of agent activity falls into categories where onchain settlement has a structural advantage over traditional rails. After applying a conservatism discount, we hold this variable at 30% across all cases. If anything, the McKinsey data suggests this is conservative. For example, B2B payments (the segment most analogous to agent-to-agent commerce) already represent $226 billion, or roughly 60% of all real stablecoin payment volume in 2025.

Today, Solana captures more than a third of AI agent transactions and more than 50% of x402 payment volume depending on the day. Our 30% long-term assumption implicitly assumes competitive erosion as Base, Ethereum L2s, and potentially purpose-built agent chains absorb share. This may prove conservative, but we prefer to model competitive pressure rather than assume dominance persists indefinitely.

Bear: 20% (meaningful competition from Base and Ethereum L2s erodes Solana’s first-mover advantage).

Base: 30% (competitive erosion partially offset by Solana’s speed and cost advantages).

Bull: 45% (Solana’s infrastructure moat, including the Alpenglow upgrade targeting 150ms finality, proves durable; network effects compound).

Variable 4: SOL Holding Ratio (15%)

This variable captures the share of onchain agent activity that must be held as SOL at any given time, across gas pre-funding, operational wallets, priority fee reserves, DeFi positions, and account rent. Per agent, the requirement is small. But in aggregate, it scales with the number of agents.

The key insight here is that gas is not the primary SOL demand driver for agents. Agents interacting with DeFi need SOL in their positions (LP pairs, collateral). Agents competing for execution priority need SOL for priority fees. Agent platforms need SOL for account rent and program deployment. And gas abstraction (where a relayer pays SOL on behalf of an agent paying in USDC) does not eliminate SOL demand. Instead, it shifts it to infrastructure providers who must hold SOL themselves. The net system-wide SOL requirement is similar; the distribution changes.

That said, if gas abstraction matures and most agent activity consists of simple API payments (x402-style) with minimal DeFi interaction, the per-agent SOL float could compress materially. The bull case requires a world where DeFi-native agents dominate and hold meaningful SOL positions for trading, LP provision, and yield strategies.

Bear: 8% (gas abstraction compresses the operational layer; most agent activity is simple API payments with minimal DeFi interaction).

Base: 15% (mix of DeFi-active agents and simple API consumers).

Bull: 25% (DeFi-native agents dominate; agents hold meaningful SOL positions for trading, LP provision, and yield strategies).

Sensitivity Analysis

The table below shows implied SOL demand under different assumption sets. All figures assume 30% onchain migration unless otherwise noted.

Several things stand out. First, even the bear case ($6.8B) produces meaningful demand relative to today’s nearly-zero baseline. Second, the range is wide: $6.8B to $112.5B, a 16.5x spread. This reflects the genuine uncertainty about how large the agent economy becomes, not uncertainty about whether agents will use SOL (they already do). Third, our base case of $27B implies that agentic AI alone would support meaningful SOL price appreciation before any contribution from the other three demand buckets. Running our DFDV model with only the Agentic AI bucket turned on (i.e., assuming zero demand from RWAs, stablecoins, and consumer activity) implies a SOL price of $360.

An Alternate Lens: Agent Count as the Demand Driver

The four-variable framework above is useful for stress-testing assumptions, but it can feel abstract. Here we offer a complementary way to think about the same question: how many agents need to exist for the demand figures above to hold?

Every agent operating on Solana requires some baseline amount of SOL. A simple API-payment agent needs a wallet rent deposit (~$0.08), token accounts for USDC and other SPL tokens (~$0.52 assuming three accounts), a gas pre-funding buffer sufficient for several days of activity (~$1.50), and a priority fee reserve (~$0.75). That's roughly $2.85 in operational SOL per agent at the floor. Agents that interact with DeFi (by providing liquidity, posting collateral, competing for execution priority, etc) hold materially more: $50–$150+, depending on the strategy. Blended across a population where most agents are simple (85%), and a minority are DeFi-native (15%), we estimate approximately $25 in SOL per agent at baseline.

If per-agent SOL demand were static, the relationship between agent count and total demand for SOL would be linear. It isn't. Two compounding forces make the curve super-linear:

Network effects on per-agent demand: First, as the agent population grows, each agent transacts with more counterparties. More services become x402-payable, more DeFi pools deepen, and more agent-to-agent payment corridors open, which in turn increases the per-agent SOL float required to operate. We model the network effect using a square-root function: per-agent demand scales with √(N / 1,000,000), where N is the total agent count. This is a conservative form of Metcalfe’s Law.

DeFi composition shift: Early agent populations are mostly simple (API payments, data purchases, aka low SOL intensity). As the ecosystem matures, DeFi-native agents (MEV, LP provision, yield optimization) grow as a share of the mix. We assume DeFi-native agents hold roughly 50% more SOL on average because they need LP positions, collateral, and priority fee reserves that simple agents do not.

The full equation is:

Total SOL Demand ($) = $25 * N * √(N / 1,000,000) * (1 + 0.5 * DeFi Share)Where:

N represents the number of active, onchain Solana agents

$25 is the base per-agent SOL cost

√(N / 1,000,000) captures the network effects on per-agent demand

DeFi Share represents the percentage of the total onchain Solana agent population that consists of DeFi-native agents (MEV bots, liquidation agents, LP managers, yield optimizers) as opposed to simple agents (API payments, data purchases, x402 micropayments).

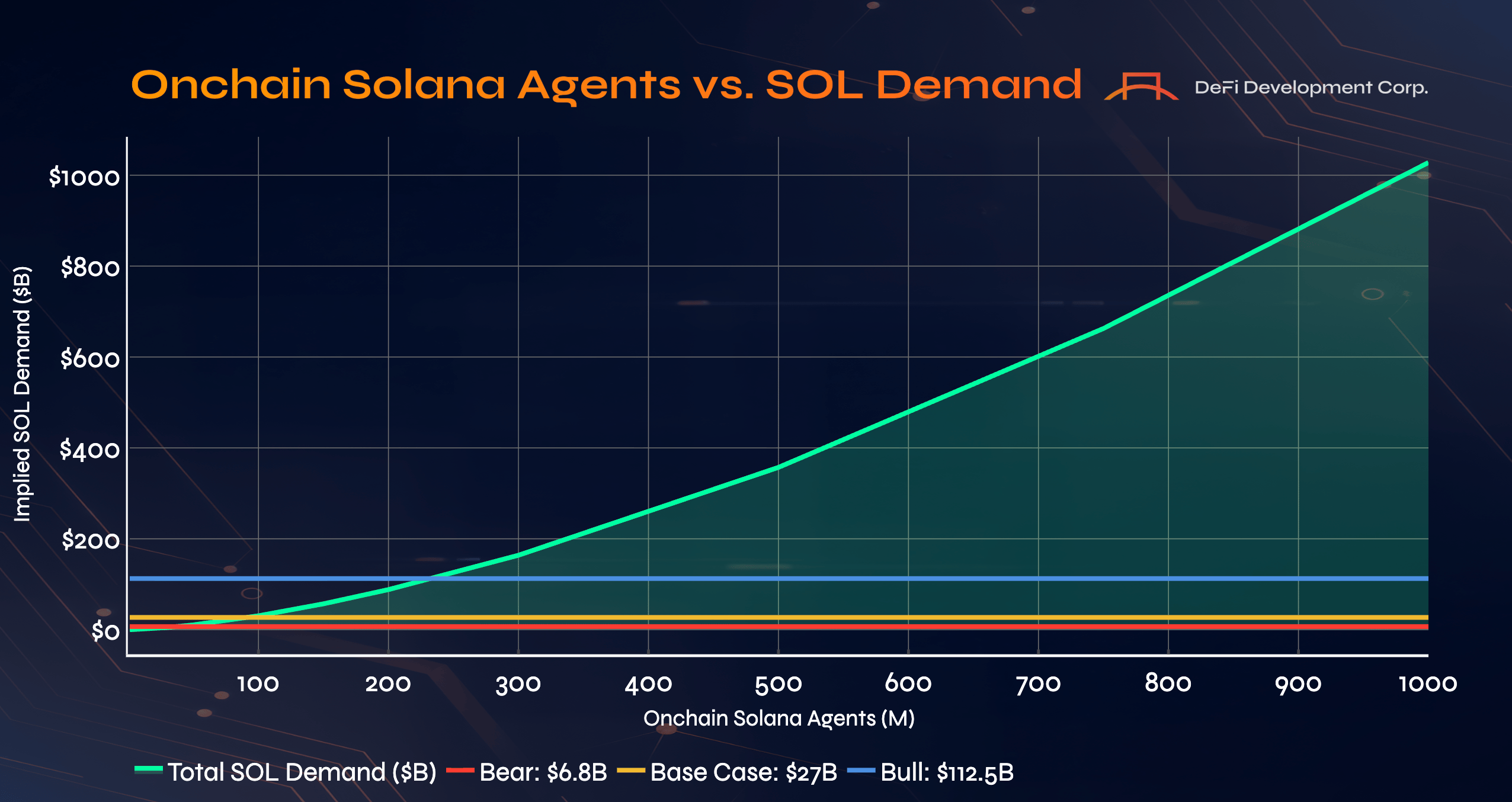

The resulting curve is super-linear. At 10 million agents on Solana, implied SOL demand is roughly $900 million. At 95 million, it reaches approximately $27 billion, matching our base case. At 250 million, it exceeds $100 billion. The chart below plots this relationship with reference lines at the bear, base, and bull case scenarios from our sensitivity table.

The key question then becomes: Is 95 million active onchain Solana agents plausible? Gartner projects 40% of enterprise applications will embed AI agents by the end of 2026, up from less than 5% today. Our model assumes 30% of the agent economy moves onchain and Solana captures 30% of that, implying that 95 million onchain Solana agents map to a total global agent population of roughly 1 billion. That may be aggressive for 2026, but well within reason over a longer horizon. The chart makes this threshold visible: readers can decide for themselves whether the AI agent population will reach the levels required to justify each scenario.

Risks and Barriers to Adoption

We see four risks that could cause the agentic demand bucket to underperform.

Security

Autonomous agents with access to wallets, files, and APIs present a large attack surface. Cisco’s security team found critical vulnerabilities in OpenClaw, including data exfiltration and prompt injection via third-party skills (Cisco Blogs). Palo Alto Networks described OpenClaw as “the potential biggest insider threat of 2026.” Anthropic’s research found that AI agents successfully exploited 207 of 405 smart contracts in a simulated environment (The Block). If agents cannot be trusted with meaningful capital, the demand ceiling shrinks dramatically.

Reliability and Trust

Information Matters reports that while 38% of users trust agents for routine data analysis, only 20% trust them for high-stakes financial transactions (Information Matters). This trust gap must close for agents to handle meaningful economic activity. The “centaur phase” (human-AI collaboration rather than full autonomy) may persist longer than bulls expect.

Regulatory Uncertainty

Agents that autonomously execute financial transactions raise novel questions about liability, compliance, and consumer protection. Regulators have not yet addressed whether an agent-initiated trade constitutes a securities transaction, who is liable when an agent makes a harmful decision, or how AML/KYC requirements apply to machine wallets. Regulatory ambiguity could slow the adoption of onchain agent workflows.

Circularity of Early Data

Much of the observable agent economic activity today is endogenous to crypto: agents trading tokens, providing liquidity on DEXs, and competing for MEV. The $31B AI agent DEX volume is largely this kind of activity. The structural demand thesis in our model depends on agents paying for exogenous goods and services (i.e., data, compute, real-world APIs, non-crypto commerce), not just recycling value within the crypto ecosystem. x402 is the clearest evidence of exogenous demand (agents buying data and API access from non-crypto providers), but cumulative real (non-gamed) x402 volume remains modest. If agent activity remains predominantly endogenous, the effective SOL demand is lower than our model implies because the value is circular rather than additive.

Near-Term Catalysts

Alpenglow Upgrade (2026): Solana’s largest-ever consensus overhaul targets ~150ms finality, a 10x improvement. For agents operating in tight feedback loops, this further widens Solana’s latency advantage over every competitor.

x402 Ecosystem Growth: Stripe launched x402 payments on Base in February 2026. Cloudflare, Google, and Vercel are active supporters. As more services become x402-payable, the addressable activity for onchain agents expands. Galaxy Digital projects x402 could reach 5% of Solana’s daily transactions in 2026.

Agent Wallet Infrastructure: Coinbase launched “Agentric Wallets” in February 2026, specifically designed for AI agents to autonomously hold funds, trade, and pay for services. This institutional-grade infrastructure lowers the barrier for enterprise agent deployment.

Conclusion

The agentic AI demand bucket in the DFDV model rests on a simple thesis. As the number of autonomous agents grows and these agents transact onchain, they create a persistent, structural demand for SOL. The demand is small per agent, but compounds across millions (and eventually billions) of agents.

The observable data supports this thesis, including $31B in AI agent DEX volume on Solana in 2025, over 170M cumulative x402 transactions, and 50%+ of AI agent volume captured by Solana. That said, the early data carries important caveats: much of the DEX volume is speculative trading in AI-associated tokens rather than autonomous economic activity, and the x402 numbers, while cleaner, are still small in absolute terms.

The uncertainty is in the scale: will the global agent economy reach $500B or $5T? Will Solana hold 20% share or 45%? Will agents hold 8% or 25% of their activity as SOL? The base case ($27B) is defensible given current trajectories. But the asymmetry is notable: even the bear case produces billions in demand, while the bull case produces over $100B. The downside is a bucket that contributes modestly to the DFDV model. The upside is a bucket that rivals or exceeds the demand from stablecoin settlement reserves.

Addressing Concerns

If agent transactions are fractions of a cent, isn't the TAM tiny?

This is sizing the wrong TAM. The revenue opportunity from processing agent payments is small, we agree. But that's not what this report is sizing. We are forecasting the aggregate SOL that must be held across the network to support agent activity: gas, priority fees, account rent, DeFi positions, and operational float. Agent transactions are small individually. But millions of agents transact thousands of times per day, each holding working capital in SOL to operate, producing meaningful aggregate demand for the native asset. The value accrues to SOL holders, not payment processors.

Agents transact in USDC, not SOL. Why does 15% of their activity need to be held as SOL?

It doesn’t, for most agents. The 15% is a blended figure across a population that includes both simple API-payment agents (whose SOL requirement is for gas, rent, and priority fees) and DeFi-native agents (whose SOL requirement is much higher for LP positions, collateral, and execution priority). The blend is pulled up by the DeFi minority. In a world where gas abstraction matures, and most agents are simple x402 consumers, the effective ratio compresses. If the ratio lands at 5%, the demand level drops from $27B to $9B. While smaller, this amount is still meaningful relative to today’s near-zero baseline.

The 30% onchain variable has no external validation. How confident are you in that number?

The segment shares (40/25/20/15) and onchain probabilities (5/60/70/100) in our bottom-up framework are DFDV estimates, not externally sourced figures. The variable most likely to move the blend is the size of the intra-enterprise segment. If internal automation represents 55–60% of the agent economy rather than 40%, the pre-haircut blend drops to roughly 30%, and the post-haircut figure falls to approximately 20%. At 20% onchain, total demand from AI agents drops from $27B to $18B. We hold Variable 2 constant across scenarios for simplicity, but it is arguably the widest-range variable in the framework.

Real x402 transactions peaked in December and declined 87% by February. Doesn’t that undermine the thesis?

Not yet, but we’re watching closely. December’s peak was inflated by infrastructure testing and incentivized activity, consistent with the high gamed share during that period. February’s lower level likely represents a more organic baseline. The real test is whether x402 V2 (released Dec 2025 with wallet-based identity, multi-chain support, and modular paywalls) and the Stripe integration in February 2026 re-accelerate adoption through 2026. If real daily transactions stabilize near current levels and fail to inflect upward over the next two quarters, the near-term observable case for agentic micropayments weakens, even if the structural thesis remains intact on a longer horizon.

Why does per-agent SOL demand scale with √N? For example, doesn’t a Visa cardholder need the same cash regardless of how many merchants accept Visa?

The √N multiplier is our attempt to capture a second-order effect: as the agent population grows, the breadth of onchain services expands, which we believe will increase per-agent transaction frequency and DeFi engagement over time. This is our own assumption, not an observed relationship. If per-agent demand is roughly constant regardless of network size, then demand will scale linearly with N rather than N^(1.5).

Where does the $360 SOL price come from? What’s the free float assumption? The $360 figure comes from our full DFDV model, which assumes approximately 75 million SOL in effective free float (total supply less staked SOL, institutional holdings, tokens in DeFi, app reserves). We detail the free float derivation in the full DFDV model documentation. The $360 figure should be read as contingent on both the demand estimate and the float assumption, not demand alone.

Disclaimer: This is for informational purposes only and reflects publicly announced developments, milestones, and media coverage related to DeFi Development Corp. (“the Company”). The information contained herein does not constitute an offer to sell or a solicitation of an offer to buy any securities, nor should it be relied upon as investment advice or a recommendation regarding any securities. Certain statements in this post may constitute “forward-looking statements” within the meaning of applicable securities laws. These statements are based on current expectations and assumptions and involve risks and uncertainties that could cause actual results or events to differ materially. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of publication. DeFi Development Corp. undertakes no obligation to update any forward-looking statements, except as required by law. All information is accurate as of the date posted and is subject to change without notice.